Fall Funfest All Breeds Horse Show - September 1st

Spectators are welcome to attend the Annual Fall Funfest All Breeds Horse Show on Sunday, September 1st from 8:00 am to 4:00 pm at the McCoy Equestrian & Recreation Center, 14280 Peyton Drive.

Lending and Mortgage news and industry updates with Crossline Capital Inc. Business Development Manager Tami Glass Fernandes

|

| |||||||||||||||||||||||||||||||

|

| Last Week in Review: The housing market continues to improve, plus the tapering talk carried on. Forecast for the Week: A busy week is ahead, with important inflation, manufacturing and housing news being released. View: Staying sharp is important for today's busy professionals. Check out the simple tips below. |

| Last Week in Review |

"Every day you make progress." Winston Churchill. And the housing market continues to progress in the right direction. Read on for details. Last week, research firm CoreLogic reported that home prices across the U.S. rose by nearly 12 percent from June 2012 to June 2013. By comparison, home prices only rose 3.76 percent from June 2011 to June 2012. In addition, research and analytics firm Clear Capital said that prices rose 9.3 percent in the year ended in July. Last week, research firm CoreLogic reported that home prices across the U.S. rose by nearly 12 percent from June 2012 to June 2013. By comparison, home prices only rose 3.76 percent from June 2011 to June 2012. In addition, research and analytics firm Clear Capital said that prices rose 9.3 percent in the year ended in July.The housing markets have turned the corner to greener pastures, but it's important to note that this pace of growth may be unsustainable. With home loan rates rising over the past several months, this rate of appreciation could slow. In labor market news, Weekly Initial Jobless Claims rose by 5,000 in the latest week to 333,000, but this was below the 340,000 expected. This followed the Jobs Report for July, which was a bit of a disappointment with less jobs created than expected. What does this mean for home loan rates? One of the biggest questions on everyone's mind is: When will the Fed start tapering their Bond purchases? Remember that the Fed has been buying $85 billion of Bonds a month to help stimulate the economy and housing market. This includes Mortgage Bonds, to which home loan rates are tied, and these purchases have helped home loan rates remain attractive. The Fed has said the rate of their purchases will continue to depend on economic data, and could be increased or decreased accordingly. Last week, several Fed members spoke out in favor of tapering these purchases as early as the Fed's meeting in mid-September. However, with our economy growing at sub 2 percent, economic data between now and September will be a key factor in this decision. The bottom line is that home loan rates remain attractive compared to historical levels and now remains a great time to consider a home purchase or refinance. Let me know if I can answer any questions at all for you or your clients. |

| Forecast for the Week |

After last week's slow calendar, this week features a steady stream of reports.

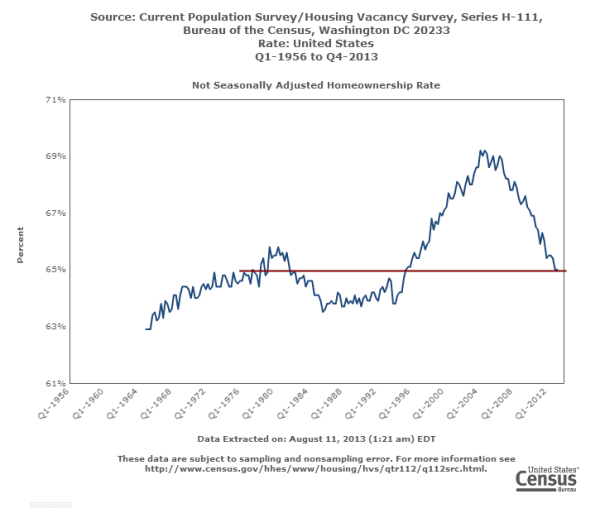

When you see these Bond prices moving higher, it means home loan rates are improving -- and when they are moving lower, home loan rates are getting worse. To go one step further -- a red "candle" means that MBS worsened during the day, while a green "candle" means MBS improved during the day. Depending on how dramatic the changes were on any given day, this can cause rate changes throughout the day, as well as on the rate sheets we start with each morning. As you can see in the chart below, Bonds have improved from multi-year lows in recent weeks. I'll be watching closely to see if they can improve further.

Chart: Fannie Mae 3.5% Mortgage Bond (Friday Aug 09, 2013)

|

| The Mortgage Market Guide View... |

| Brain Breakthroughs Many people think intellect is a matter settled at birth, and mistakenly believe there's no way to boost their brain brilliance. But scientific studies prove just the opposite. In fact, small lifestyle adjustments combined with a few mental gymnastics can not only increase intelligence, but also improve general brain health, helping prevent aging disorders, such as Alzheimer's disease. According to most neurologists, the key is staying mentally active, whatever your age. The following tips will help boost your mental acuity and increase your intelligence. All You Have To Do Is Dream. An adequate amount of restful sleep is an important component of brain function (its effect on memory and learning is contested among scientists). Restful sleep provides energy as well as the ability to focus, both vital factors in achieving mental stimulation. Some studies have also shown the reverse to be true, that is, that more mental stimulation during the day gives you better sleep at night. Jumpin' Jack Flash Memory. Exercise brings oxygen-rich blood to the brain and regulates blood-sugar levels. Exercises such as aerobics, dance, and martial arts all require memorization and are great for promoting mental stimulation. They also help to develop the rhythm and timing circuitry that runs across multiple regions of the brain. Playing Those Mind Games Together. Crossword puzzles and Sudoku, board games and card games are all excellent for mental stimulation--now you can add video games to the list. Each type of game makes various demands on brain function such as recall, hand-eye coordination, attention, memory, logic, and pattern recognition. The key here is to keep upping the skill or level of challenge as you progress. Don't forget to pass these helpful tips along to your clients and colleagues.

Economic Calendar for the Week of August 12 - August 16

|

Existing Home Sales rose by 6.5 percent in July from June and are up 17.2 percent since this time last year. In addition, the Federal Housing Finance Agency reported that home prices rose 7.7 percent in the year ended in June. From May to June, prices rose by 0.7 percent. However, New Home Sales dropped 13.4 percent in July from June, below expectations, and June's numbers were also revised lower.

Existing Home Sales rose by 6.5 percent in July from June and are up 17.2 percent since this time last year. In addition, the Federal Housing Finance Agency reported that home prices rose 7.7 percent in the year ended in June. From May to June, prices rose by 0.7 percent. However, New Home Sales dropped 13.4 percent in July from June, below expectations, and June's numbers were also revised lower.

The housing sector continues to improve despite the recent rise in home loan rates, as Housing Starts rose 5.9 percent from June to July to 896,000 on an annualized basis. This was in line with estimates. Building Permits, a sign of future construction, were up 2.7 percent, coming in above expectations. In addition, the National Association of Home Builders Housing Market Index rose to 59 in August from the 57 recorded in July. This is the best level in nearly eight years.

The housing sector continues to improve despite the recent rise in home loan rates, as Housing Starts rose 5.9 percent from June to July to 896,000 on an annualized basis. This was in line with estimates. Building Permits, a sign of future construction, were up 2.7 percent, coming in above expectations. In addition, the National Association of Home Builders Housing Market Index rose to 59 in August from the 57 recorded in July. This is the best level in nearly eight years.